When clients visit our office, we often convene in the Jack Bogle Conference Room. It’s our way of honoring the enormous contributions the late, great Vanguard founder made to investing.

What was on Bogle’s mind a decade ago?

We find the answer in his January 2010 op-ed, “Restoring Faith in Financial Markets.” In it, he roared against an industry that violated investor trust by replacing the wisdom of long-term investing with the folly of short-term speculation.

Never afraid to point fingers at his own industry, Bogle nailed the dark mood of those still reeling from the 2008–2009 global financial crisis. Investors’ fears were further fueled by popular press reminders of the “Lost Decade,” a period over which $1 invested in the S&P 500 Index shrank to just 91 cents.

Today, there may still be plenty of reasons to rail against Wall Street. But if you assumed in 2010 that the Lost Decade would continue, you were very wrong. Instead of fulfilling prevailing expectations at its outset, the 2010s largely became a decade of surprises. A decade that wasn’t.

The S&P 500 Wasn’t a Disaster

In early 2010, investors could not have known we were already 10 months into a nascent U.S. stock market rally that ended up defining the rest of the decade.

Citing “structural unemployment,” many commentators suggested the U.S. might never again prosper as it had before. In his October 2010 quarterly outlook, PIMCO’s then-revered bond king Bill Gross, citing a “new normal,” informed readers “the unmistakable fact is that future investment returns will be far lower than historical averages.” He and others further encouraged investors to get out of U.S. stocks in search of better returns in international markets.

Gross and his cronies were grossly off target. Today, unemployment is at ridiculously low numbers. And while most of the world’s stock markets grew nicely, the S&P 500 shot out the lights, nearly tripling over the past 10 years.

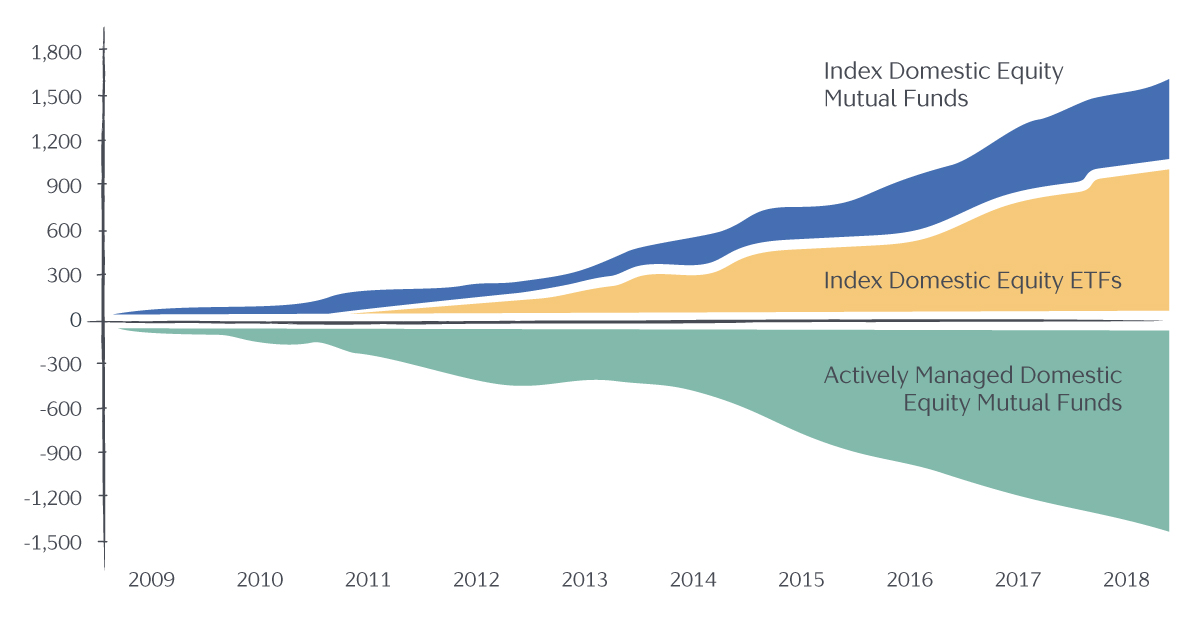

It Still Wasn’t an Active Manager’s Time to Shine

Perhaps unsurprisingly, Wall Street sought to capitalize on the pessimism. Stock pickers embarked into the 2010s by declaring active management the only hope for protection and recovery. They threw around catchy terms like “high-conviction active” and “tactical allocation,” and issued confounding declarations like, “It’s a market of stocks, not a stock market.” What does that even mean?

Thankfully, many investors increasingly wondered the same and decided to answer Wall Street’s sales pitches by voting with their feet. Since 2010, roughly $1.5 trillion has moved from active into index fund investments, as stock pickers’ records have continued to disappoint.

Rising Interest Rates Weren’t So High or Mighty After All

Remember “quantitative easing”? Starting in 2008, the Fed went on a debt buyback spree to jump-start our ailing economy.

By 2010, “nowhere to go but up” had become the popular cliché for interest rate predictions. Bracing for the expected fallout, experts glutted the news with warnings that investors should drastically shorten their bond maturities—or get out of bonds altogether—in anticipation of a massive, rising-interest-rate tide. Why lock in historically low rates?

Yet again, reality foiled that bet.

Ten years ago, 10-year U.S. Treasury rates were at 3.8%. Today, a 10-year Treasury bond yields around 1.4%, or less than half the “all-time low” from a decade ago. As bond prices move inversely to yields, this decline provided a nice tailwind to bond returns, especially those with longer maturities.

In other words, the “sure bet” on dramatic rate increases has been anything but.

Looking Ahead

So, where do we go from here? No one knows for certain.

Trade wars and immigration policies? 2020 elections? Slowdown in China? Health pandemics? All are hugely important issues, with potentially serious ramifications. But how, or if, they’ll impact your returns is unknowable.

For each crisis du jour, remember: By 2030, its impact on your investments is just as likely to be nothing as something.

Or, to echo Bogle’s timeless thoughts: “Successful short-term marketing strategies are rarely, if ever, successful long-term investment strategies.”

A far safer bet is to focus on determinants we can control: asset allocation, costs, taxes, and (most important!) our own steadfast resolve to tune out the noise.