Whether you’ve been saving for college for a while or are about to start saving, you’ll want to know about upcoming changes to Oregon’s 529 College Savings Plan.

With a new financial partner and enhanced investment options, Oregon’s 529 Plan is on track to earn top grades.

Q: What is the Oregon College Savings Plan?

A: Launched in January 2001, the Oregon College Savings Plan is a state-sponsored, tax-advantaged 529 savings plan designed to help participants save for future college costs.

Earnings grow free from federal tax, and Oregonians can deduct 529 contributions from their taxable state income – up to $4,750 in 2018 for married couples filing jointly. (Note that recent legislation disallows Oregon’s tax break for private K-12 education.)

Withdrawals used for qualified expenses are tax-free at both the federal and state levels.

Q: Who is managing the plan’s assets?

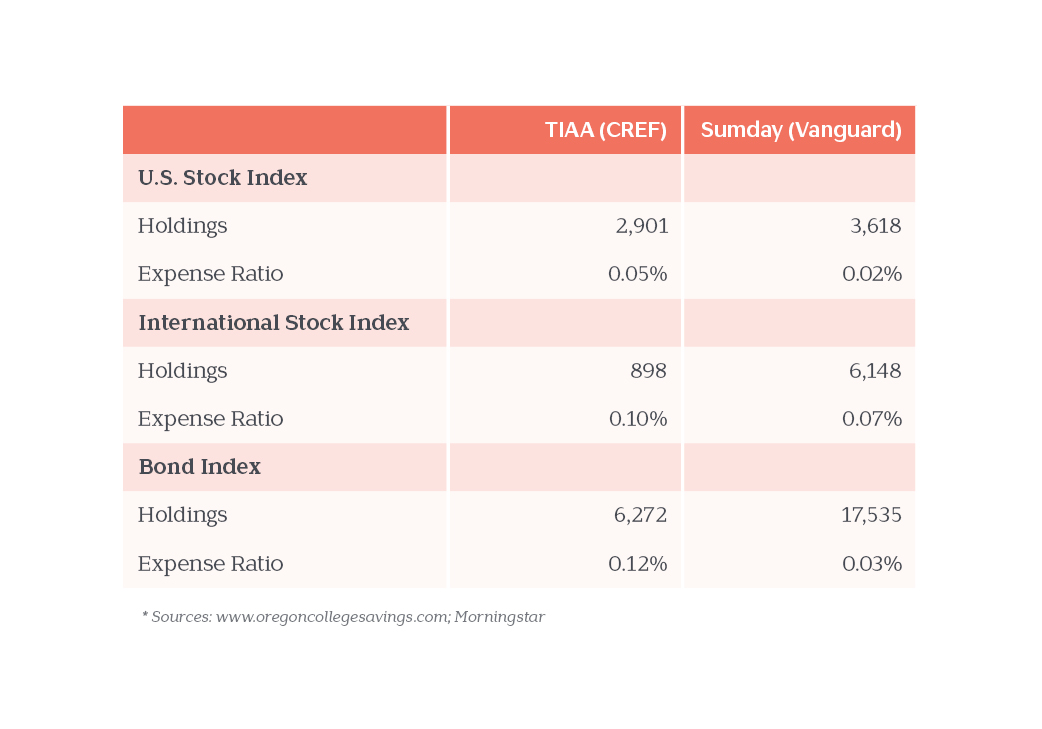

A: Sumday Administration, a subsidiary of BNY Mellon, one of the world’s largest financial institutions, will replace TIAA as the Plan’s financial partner.

We see the transition as a positive one.

Along with robust new investment options (with the same level of risk as current options), there will be a reduction in fees—from the current all-in plan fee of 0.33% to a projected all-in fee of 0.18% in 2030.

Q: Are the plan’s underlying investments changing?

A: Yes—for the better. Sumday will give plan participants access to previously unavailable DFA funds and Vanguard index funds.

This is a big win for investors. Vanguard offers greater diversification and lower costs across domestic stocks, international stocks, and bonds.

Q: I currently have an age-based Oregon 529 plan. Will this change?

A: Yes. There is a growing trend toward nontraditional education paths. Some students take a gap year, some continue on to graduate school, and still others enter school as adults.

Because not everyone starts college at age 18 or follows the same path, Oregon’s 529 Plan is moving from age-based to target date (or “enrollment date”) portfolios.

Enrollment date portfolios allow participants to better align funds with a student’s college plans and goals.

Assets will automatically be mapped over to a target enrollment date portfolio.

Q: I have auto deposits set up. Do I need to do anything?

A: If you have auto deposits set up with your bank savings or checking account, everything automatically rolls over.

If, instead, your contributions are deducted from your paycheck, you will need to complete new paperwork that notifies your employer of the change.

Where can I go for more information?

To learn more about upcoming changes, visit Oregon’s 529 College Savings Plan FAQ or contact Vista.

Live outside of Oregon? We can also help you with questions about 529 plans across the country.

This post is Part One of a three part series on Oregon’s 529 College Savings Plan. In Part Two, we share how to withdraw funds from your plan.