Retiring requires a fundamental shift from saving to spending mode. Many retirees report this transition is harder than they expected. After decades of feeding their nest egg, it seems unnatural to stop. Even worse, tapping into their savings feels like breaking a cardinal rule.

It is the details of retirement spending, however, which prove most daunting of all. Vista assists clients with this challenge by establishing sustainable withdrawal plans. Using our own, in-house planning tool, we reconcile a client’s assets, time horizon, expenses (fixed and variable) and income sources.

By running through various iterations of historical market returns and inflation rates, we can assess the viability of a plan under a wide range of real-world conditions.

This exercise involves balancing today’s needs and wants with those of future years. Spending too aggressively early on can jeopardize long-term financial independence. Spending too conservatively may unnecessarily lower quality-of-life and lead to later regret (“we could have spent more!”).

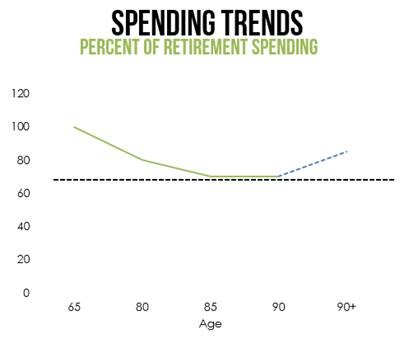

Results of a study conducted by David Blanchett of Morningstar offer useful insights for striking a healthy balance. Blanchett found that retirees who spend $100,000 annually report a 20 percent decline in spending from age 65 to age 80. By age 85, spending is reduced an additional 10 percent. These reductions in total spending are due to decreased expenditures on travel, dining out, and mortgage payments which more than offset the increase in healthcare expenses.

This means it can be possible to spend more at the outset of retirement, provided a retiree is willing and able to reduce spending in the future. Vista’s anecdotal evidence from working with retired clients for the past 16 years is remarkably similar—our clients’ spending tends to decline as they enter and progress through retirement.

A word of caution: spending more today does require a healthy dose of discipline and commitment. Clients who become accustomed to increased spending may be reluctant to ratchet back in later years. Blanchett’s study indicates that beyond age 85 is when the potential for increased health expenses is likely to occur. It is at this point that adjustments in spending habits will most likely be necessary. To what extent, however, no one can predict (represented by the dotted blue line in the graph above).

The benefit of researching retirement spending is the ability to apply more substance behind the anecdotal evidence we have acquired. Because spending can decrease in retirement by as much as 30 percent, we can adapt our approach to retirement modeling to enhance our clients’ lifestyle today, while ensuring their personal retirement well doesn’t run dry.