Happy birthday, index funds, you turned 40 last week. My, how things have changed since you were born.

It was a much-ridiculed beginning when investors entrusted just $11 million to Jack Bogle’s Vanguard index fund back in 1976. In the forty years since, investor demand for index funds—which aim to reliably deliver the returns of market averages—has grown dramatically. In the last year alone, more than $400 billion of net new cash has flowed into index funds. Today, they hold more than $4 trillion of U.S investor savings. Uncork the champagne, Mr. Bogle.

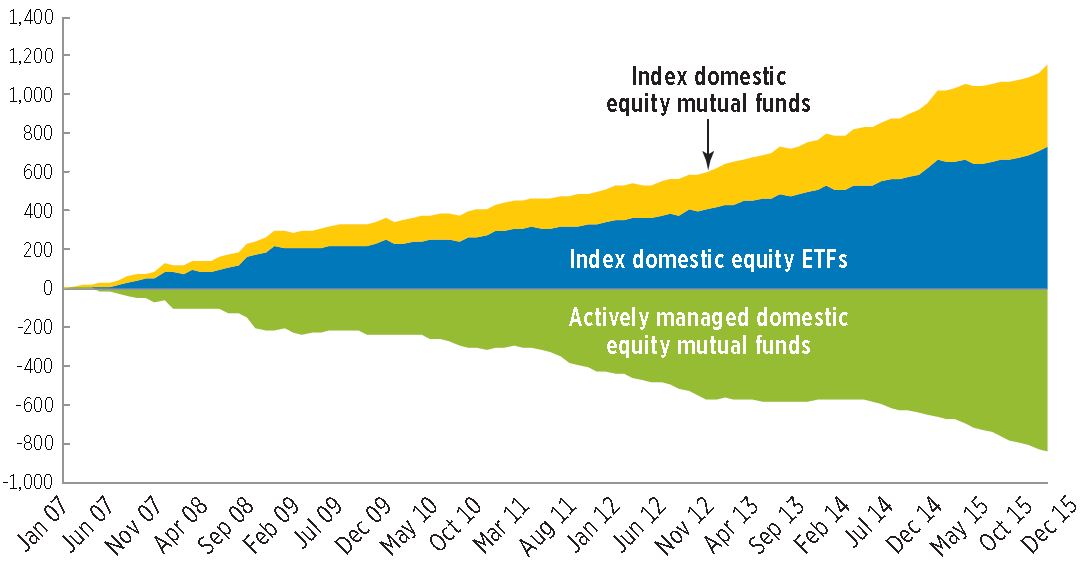

Not everyone, however, is ready to celebrate. The windfall for index funds has come largely at the expense of Wall Street’s active managers. Since 2007, of the nearly $1.2 trillion flowing into index funds, roughly $900 billion has come from actively-managed fund redemptions.

Outflows from Active Funds to Index Funds and ETFs

Cumulative net flows, in $ billions

Source: Investment Company Institute 2015 Factbook

This giant sucking sound has Wall Street managers foaming at the mouth. Renowned hedge fund manager Bill Ackman has called the recent trend an “index bubble.” Others have claimed index funds are “un-American” and border on “socialism.” The most recent outcry comes from research firm Sanford Bernstein, which garnered attention by suggesting indexing was “worse than Marxism.”

Bernstein’s allegations aim to highlight the role active managers play in a capitalist society. Indeed, it is the competition amongst these highly-trained, hard-working and exceedingly-motivated active investors that helps determine security prices and keeps markets efficient. But Bernstein’s claim that a rise in indexing will distort markets and erode the foundation of capitalism borders on ridiculous.

We’re a long way—a laughable proposition, says Bogle—from a world in which index funds dominate markets. According to the Investment Company Institute, assets in index funds account for just 22% of all U.S. mutual fund assets and barely one-tenth of worldwide fund assets. Keep in mind, U.S. mutual funds hold just 30% of all publicly-traded stock in this country.

In other words, index funds hold just a fraction of the total investable U.S. stock market, and even less of the world market. According to a Vanguard spokesman, on a typical day, only 5% to 10% of total trading volume comes from index funds. There’s still plenty of active management.

So what’s the real implication of the rise of indexing?

Remarkably, it makes the case for embracing index funds even stronger. As index funds grab an ever-larger share of the market, it’s likely to become even harder for remaining active investors to outperform. Since winning active investors do so only at the expense of other active investors who lose, the shrinking pool of active investors should have a harder time finding easy pickings.

Recent data confirms just how difficult it is. Standard & Poor’s, for example, found that 91% of active managers in emerging market stocks—often thought to be the most fertile domain for experts who try to hand pick winners—failed to beat the relevant index over the past ten years. This caused the CEO of a global association of investment managers to remark, “the tide has gone out and the emperor has no clothes.”

Index funds’ 40th birthday celebration should, therefore, also be a coronation. Index funds have clearly won. But given how much money the active management industry extracts from investors’ wallets each year, cries of “index bubbles,” “Marxism” and other ridicule will likely continue. Let’s not allow such hyperventilating to distract us from celebrating the real gift index funds have provided investors.