Recently, Federal Reserve officials announced they anticipate raising short-term interest rates later this year. This news is likely to renew fears for bond investors, as bond prices move in the opposite direction of interest rates.

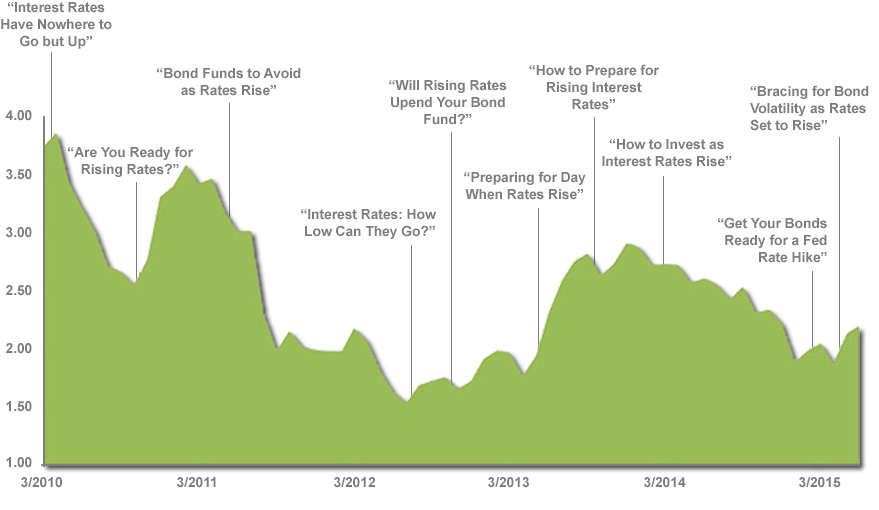

While announcements from the Fed may be more credible than headlines in the media, various experts (including past Fed policy makers) have predicted interest rates would increase for many years now. As far back as 2010, market observers have claimed rates have nowhere to go but up. To protect portfolios from rising rates, they said, investors should shift from bonds with longer maturities to those with short-term maturities, which decline less in price as rates rise.

The graph illustrates the month-end yield for the 10 Year U.S. Treasury Bond, as provided by the Federal Reserve Bank of St. Louis. The vertical axis is the yield, in percentage points, of the 10 Year U.S. Treasury Bond. The events highlighted are not intended to explain market movements.

As the graphic above shows, however, interest rates have actually declined since 2010. Investors who fell prey to the headlines most certainly left money on the table, as one-month Treasury bills have returned an annualized 0.1% since 2010 while long-term U.S. government bonds have returned 9.9% per year.

What if policy makers are correct this time and interest rates finally do increase? Does this spell disaster for bond holders?

No. In fact, higher bond yields are good news for bond investors in the long run. Yes, rising rates will temporarily hurt bond returns, as their value declines with increasing yields. But over a longer horizon, a diversified bond fund will benefit from rising rates as bonds that mature are replaced with new bonds offering the higher rate of interest. The effect of higher rates over time more than compensates for the initial price decline. In other words, “short-term pain, long-term gain.”

For those still concerned about what the future holds for bonds and interest rates, we offer two thoughts:

First, the phrase “short-term pain” is a relative one. Looking back to 1926, the worst 12-month return for intermediate-term Treasury bonds (similar to those anchoring Vista portfolios) was -6%. For comparison, the lowest 12-month return for U.S. stocks was -65%. Clearly, a bear market in bonds is a much different animal than a bear market in stocks.

Second, let’s remember why we own bonds in the first place. Bonds are not held in a portfolio for extra return, but rather to act as a shock absorber during periods of extreme market distress for stocks.

A vivid example of this occurred in 2008. As investors around the world fled stocks in pursuit of safety, high-quality government bonds—particularly U.S. Treasuries—provided much-needed ballast to portfolios. While riskier corporate bonds, high-yield bonds and dividend-paying stocks fell 5%, 26% and 34%, respectively, intermediate-term U.S. Treasury bonds increased by 11%.

Having a portfolio asset which is maintaining, if not improving, in value during such extreme and difficult periods protects investors from one of the biggest, yet most common, mistakes: giving up on stocks entirely and selling when prices are down.

No investment has offered this protection better than high-quality government bonds, and nothing appears safer today.