Memories fade fast, but 2014 was a good year. The U.S. had the highest rate of job growth since 1999, world hunger reached a new low, and it was another tax-friendly year for Vista portfolios.

Not so for many mutual fund shareholders, who found themselves on the receiving end of large tax bills.

In 2014, over 500 mutual funds distributed capital gains of more than 10%. Another 60 funds made distributions over 20%. Capital gain distributions generally result from Wall Street fund managers’ hyperactivity—darting in and out of stocks throughout the year—and reduce the net returns which end up in investors’ pockets.

In contrast, the funds in a typical Vista portfolio saw little to no year-end capital gain distributions last year. Since the funds we favor in client portfolios are primarily index and asset class funds, trading activity is relatively limited.

Less frequent trading helps drive down trading costs and reduces the potential for realized capital gains. The result is our clients can expect to keep more of the returns their investments generate.

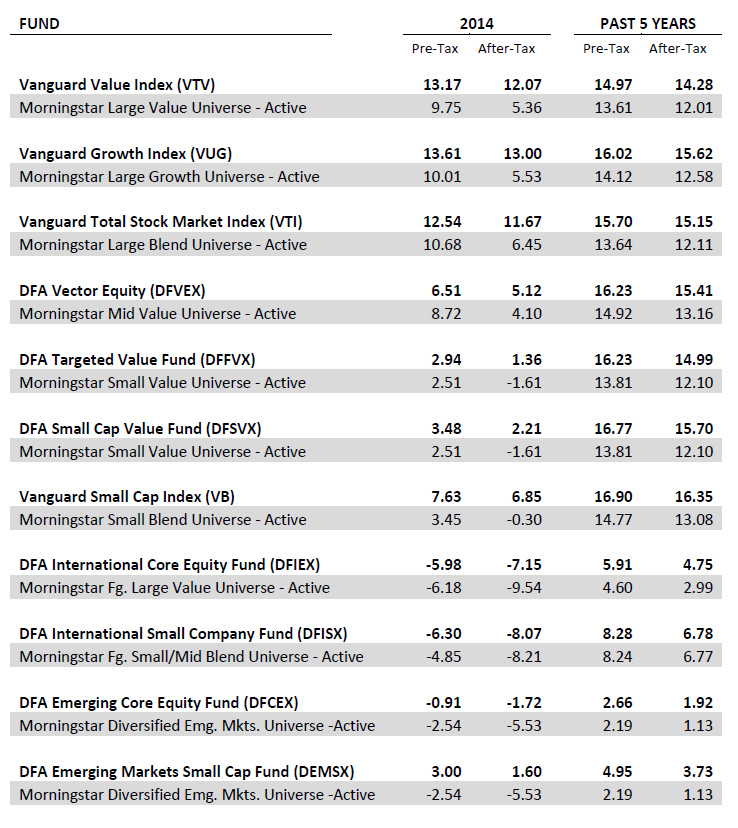

The table below shows historical pre-tax and post-tax returns for several stock funds we prefer, relative to a comparable universe of actively-managed funds. For every fund in every period shown, the post-tax return is higher than the return of its peer group.

Source: Morningstar and Dimensional Fund Advisors. Past 5 Years’ returns are annualized. Post-tax returns reflect taxes owed on income, dividends and capital gain distributions. Post-Tax returns are shown pre-liquidation, calculated using the highest individual federal marginal tax rates, and do not reflect the impact of state and local taxes. An actual investor’s tax situation may differ. Post-Tax returns are not relevant to investors who hold shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts. Active is defined as any non-index fund.

What matters most, of course, is the return which ultimately ends up in an investor’s pocket. For taxable accounts, that’s the post-tax return; for tax-deferred accounts, the focus should be on pre-tax returns. That’s why we—whenever possible—hold funds with higher relative tax costs in tax-advantaged accounts.

Being ever mindful of the role taxes play in performance may lack the sizzle peddled by Wall Street, but it does allow us to look back on 2014 and say, “Now, that was a good year.”