Since 2010, U.S. large company stocks have appreciated more than 100%. Large cap stocks in international developed and emerging market stocks are up “just” 32% and 16%, respectively. With foreign shares underperforming U.S. stocks again last year, some investors may question the value of international diversification. They shouldn’t.

It’s important to remember stock represents an ownership interest in an issuing company. This is true whether that company is headquartered in Delaware or Denmark. The fundamental risk of owning a stock is the same across geographic markets, which is why it’s reasonable to expect similar long-term returns for U.S. and international stocks.

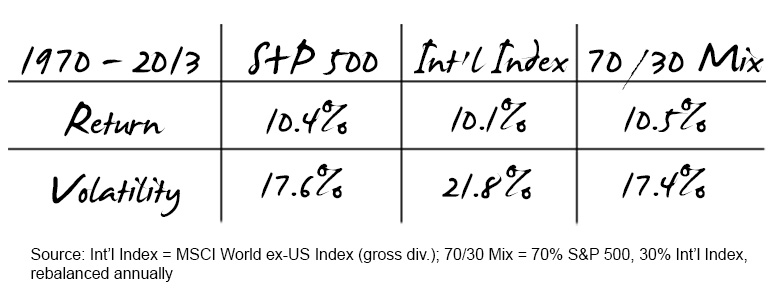

Combining these two asset classes, however, is where the magic happens. Diversification is the “free lunch” in investing whereby two investments with similar long-term returns—but which don’t move in perfect sync with each other—produce higher returns with less risk (volatility) together than either does individually. As the table below illustrates, a sensible allocation to international stocks would have improved the results of an all-U.S. stock portfolio over the past 40+ years.

U.S. stocks and international stocks each represent an important asset class in a portfolio, although their inevitable periods of disappointing performance may cause investors to wonder why they own either from time to time. That time seems to be now for international stocks. But just as it would have been unwise to give up on U.S. stocks at the end of 2007 after a six year stretch during which domestic shares underperformed international ones by a cumulative 100%, it is likely ill-timed to give up on foreign stocks today.

When constructing portfolios, we look beyond popular large company stocks in both U.S. and international markets. A typical Vista portfolio has more than half of its international stock exposure in smaller and lower-priced companies, and nearly one-third invested in emerging markets. These companies tend to do more business in their local markets, so are less influenced by the economic currents which affect larger U.S. and developed international companies. This is a diversification benefit and—since smaller and less-pricey stocks have historically delivered higher returns than large growth stocks—is expected to provide a performance advantage, as well.

We don’t know how long the relative underperformance of international stocks will continue, but we do know that reacting to short-term trends is a loser’s game. An allocation to international stocks, focused on small cap, low-priced and highly-profitable companies, continues to be an important part of our clients’ portfolios. Maintaining discipline through the inevitable ups and downs of any asset class ensures our clients benefit from the free lunch diversification provides.