In today’s low-yield environment, dividend-paying stocks have become a popular choice. But are income investors really better off with this coupon-clipping alternative?

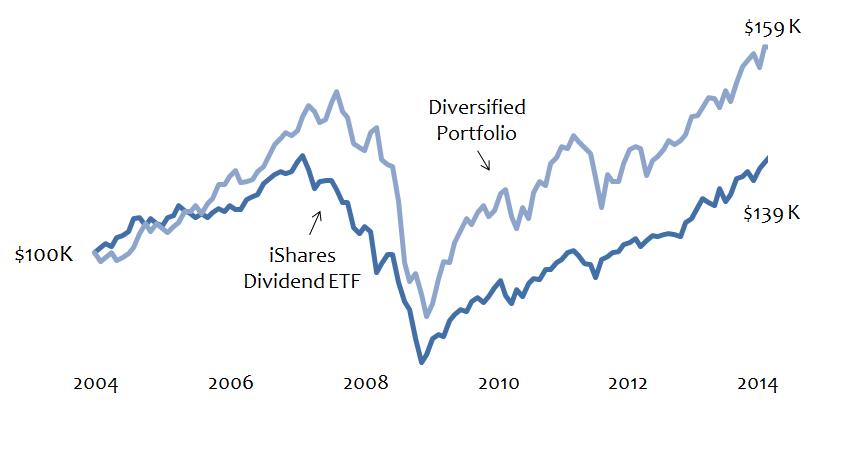

To address this question, we compared two $100,000 portfolios over the past ten years; one invested entirely in a high-dividend strategy, the other in a index fund portfolio comprised of 60% U.S. stocks, 30% international stocks, 10% real-estate investment trusts (REITs). To replicate a dividend strategy, we used data from the iShares Select Dividend ETF (ticker: DVY), since it is one of the largest dividend funds, by assets, and is the only dividend fund with at least a 10-year history.

Dividends from the DVY, and an equal amount from the diversified portfolio, were withdrawn each year. Since annual dividends from the DVY portfolio were greater, some principal was withdrawn each year from the diversified portfolio to make up the difference. Creating such “homemade” dividends via asset sales in the diversified portfolio are functionally equivalent to dividends from DVY as, of this writing, tax rates for qualified dividends and long-term capital gains are the same.

Over the ten year period, the two portfolios produced identical cash flow, but what about their ending values? Despite dipping into principal each year, the diversified portfolio value ended $20,000 higher than the DVY portfolio.

These findings suggest a total return approach based on a well-diversified portfolio may be superior to a singular focus on dividends. A total return approach relies on multiple asset classes to generate cash flow: Dividends (from stocks and REITs), capital gains and the occasional return of principal (each from asset sales).

What’s more, cash flow under a total return approach can be prudently generated regardless of the dividends stocks provide in any given year.