Fueled in part by historically-low mortgage interest rates, sales of new and existing homes have surged recently. In 2013, new home sales hit their highest annual level in five years, according to the Commerce Department.[1]

Separately, the most recent S&P Case-Shiller index showed existing-home prices in twenty U.S. metropolitan areas were 13% higher than a year earlier.[2]

These increases have renewed investor optimism for residential real estate. According to Yale professor Robert Shiller, however, folks shouldn’t get too excited. “One year home prices increases, after correcting for inflation, have had almost no statistical relationship to increases 10 years down the road.” In other words, the past year’s gains don’t tell us much about where prices are headed.

We do know homes have not made a great investment in the past. In fact, prices have barely budged over the long-haul, at least in real terms. Over the 100 years ending in 1990, home prices—adjusted for inflation—rose only 0.2% per year, according to Shiller. His explanation for the paltry gains? Rising productivity in construction which offset increases in land and labor costs.

Keep in mind inflation has historically run about 3% per year. If productivity gains and inflation continued their long-run trends, today’s $500,000 house would sell for $685,000 a decade from now. A nice dollar gain at first blush—until you consider the price is virtually unchanged in real terms.

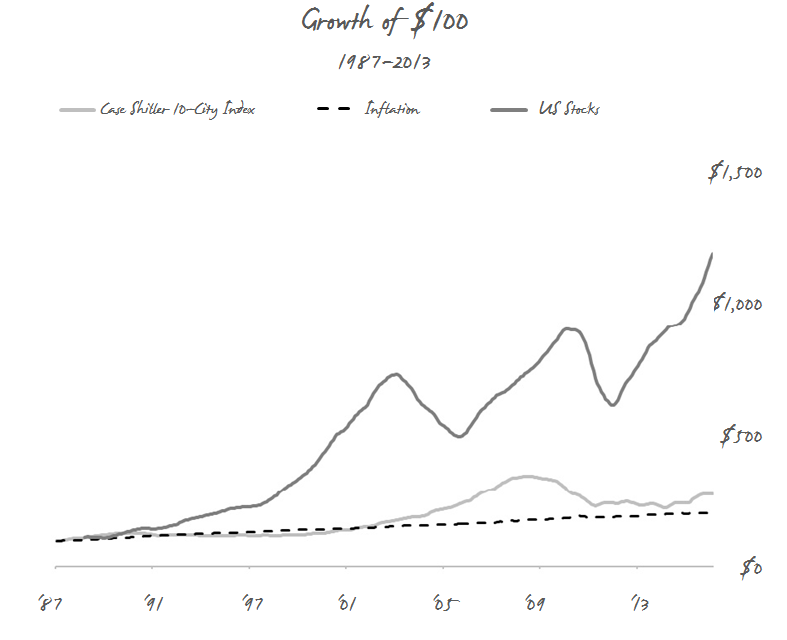

It should come as no surprise homes have had difficulty competing with stocks as an investment. Homes are a depreciating asset, the real prices of which decline over time absent maintenance and improvements. In contrast, company earnings not paid out as dividends can be plowed back into the business. As businesses grow, real stock prices should also grow.

While many folks have created significant wealth via their homes, most of those gains are likely due to leverage (borrowing up to 80% of a home’s cost). Yes, real estate prices can move sharply in both directions, providing an opportunity for savvy investors. Capitalizing on those opportunities, however, requires the ability and willingness to only buy a home when the price is right (low), and to sell (move out) if prices rise too far too fast.

Absent this discipline, a house is primarily a roof over your head and a great place to raise the kids.

________________________________________

[1] “Home Prices Defy Weak Sales Numbers According to the S&P/Case-Shiller Home Price Indices.” S&P Down Jones Indices. April 29, 2014.

[2] Shiller, Robert. “Why Home Prices Change (or Don’t).” The New York Times. April 13, 2013.