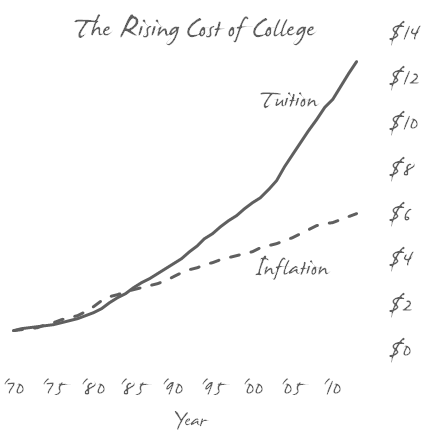

The cost of a college education continues to rise faster than general inflation, making saving for a child’s future education a daunting task. Fortunately, state-sponsored college savings programs known as “529 plans” help families meet this challenge.

A 529 plan receives preferential tax treatment and investment options include mutual funds that invest in stocks, bonds, and cash. The funds can be withdrawn tax-free for qualified higher education expenses such as tuition, room/board, books, supplies and equipment. Tax-free growth is powerful when compounded over 18+ years.

Account owners, typically parents or grandparents, can open a 529 plan in any state, however, the account beneficiary may attend any accredited college in the US or abroad. If the beneficiary chooses not to attend college or does not use the entire account balance, the account owner can change the beneficiary to another family member of the beneficiary. This allows the account owner to avoid a “non-qualified” withdrawal where the investment earnings would be subject to federal income taxation and an additional 10% penalty. Furthermore, a plan’s asset allocation can be changed or the balance transferred from one state’s plan to another.

Nearly every state offers a tax-advantaged 529 college savings plan, each with its own set of investment choices, costs and potential state tax incentives. Because of its state tax benefits, the Oregon College Savings Plan can be a great choice for Oregon residents. Utah’s Educational Savings Plan deserves mention due to its broadly-diversified fund choices and rock-bottom costs. After all, the less you pay, the more you keep

For more information regarding these and other 529 plans, please visit savingforcollege.com