Think identifying the next Apple or Microsoft is difficult? Try being a diversified investor—now that’s really tough.

Diversified portfolios are simply those comprised of numerous asset classes, the individual results of which don’t move in lockstep with each other. Combining such asset classes can result in a portfolio with higher returns, or less risk, than a concentrated portfolio. Harry Markowitz earned a Nobel Prize for presenting the mathematics behind why this is true. Yet no math is needed to understand the basic concept: Don’t put all your eggs in one basket.

If diversification is such a no-brainer in theory, why can it be so painful in practice? Because there is always a part of your portfolio you despise.

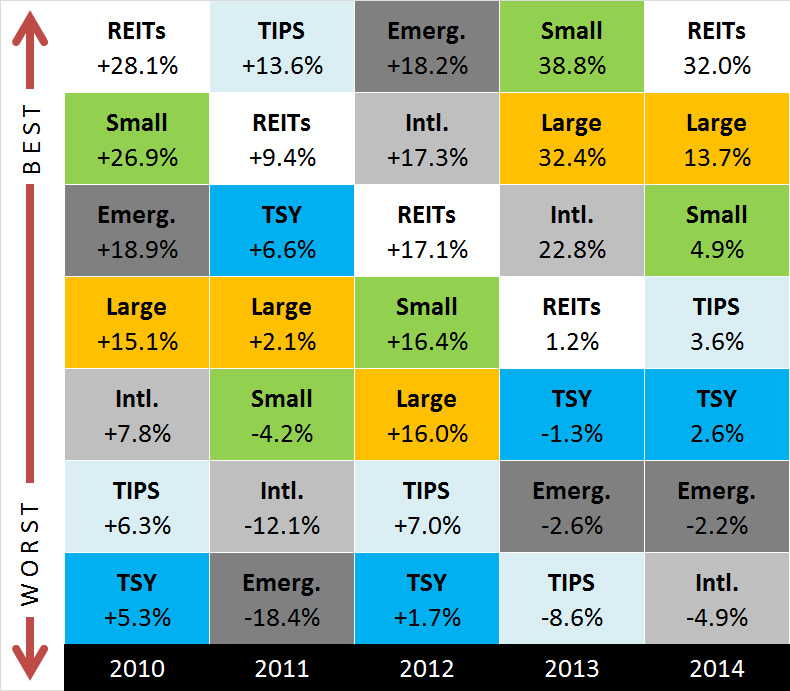

Consider the past five years. Despite being a strong period overall, returns of the selected asset classes shown below have varied dramatically.

Note: Large = S&P 500, Small = Russell 2000, TSY = Treasury Bonds

Every year part of a diversified portfolio is guaranteed to perform worse than another. In 2013, for example, the return differential between the best and worst performing asset classes was nearly 50%. Often times, part of the portfolio will actually lose money. In three of the past five years, at least two of the asset classes shown above posted losses. Such wide disparity in results provides ample opportunity for feelings of pain and regret.

These feelings, of course, are perfectly normal. Psychologists have documented several behavioral biases, a few of which are particularly relevant to investors holding diversified portfolios:

• Loss Aversion—the pain we feel with losses is about twice as aggravating as is the joy associated with gains. This means we need to win about $200 to offset the pain of losing $100.

• Fallacy of Composition—we tend to believe the portfolio as a whole is not doing well if one part of it is performing poorly. While an equally-weighted portfolio of the assets above returned an impressive 9.3% per year over the past five years, an investor may view this less favorably due to the lackluster results of one of its individual components.

• Recency Bias—we believe what’s done well/poorly in the past will continue to do well/poorly. The perils of “rear-view investing” are real. One million dollars invested in a diversified portfolio of the asset classes shown above grew to $1,560,000 from 2010 to 2014. A portfolio comprised solely of the prior year’s best performing asset grew to only $1,420,000.

• Hindsight Bias—is the inclination to believe, after an event has occurred, that we could have foreseen it. With all the attention that’s been paid to the underperformance of international stocks, it’s natural to fool ourselves into believing we “saw it coming” or “knew it all along.”

Left unchecked, these natural behavioral biases can wreak havoc on investors’ wealth. A diversified portfolio is the surest path to long-term investment success. It’s proven mathematically and reinforced by common sense.

But it sure isn’t easy. Owning temporary underperformers—even outright losers—is built into the definition of the word. Indeed, periods of pain are the norm when a portfolio is properly diversified.

To give up when they invariably pop up, however, would result in the greatest pain of all: Failure to realize our goals and ambitions.